OFAC’s GL 5W and GL 58: Venezuela’s Debt Moves From Litigation Freeze Toward Restructuring Preparation

IQLatino DC/Caracas Desk – The U.S. Treasury’s Office of Foreign Assets Control issued two Venezuela-related general licenses this week that, taken together, clarify Washington’s near-term approach to Venezuela’s debt and asset question. General License 5W, issued May 4, extends the delayed effectiveness of the authorization related to the PDVSA 2020 8.5% bond until June 19, 2026. General License 58, issued May 5, authorizes certain legal, financial advisory, and consulting services to the Government of Venezuela, PDVSA, and PDVSA-controlled entities in connection with a potential debt restructuring.

The practical message is clear: Washington is preserving protection around CITGO while allowing the technical design phase of a Venezuelan debt restructuring to begin. This is not yet a full restructuring license. It is a controlled opening for preparatory work.

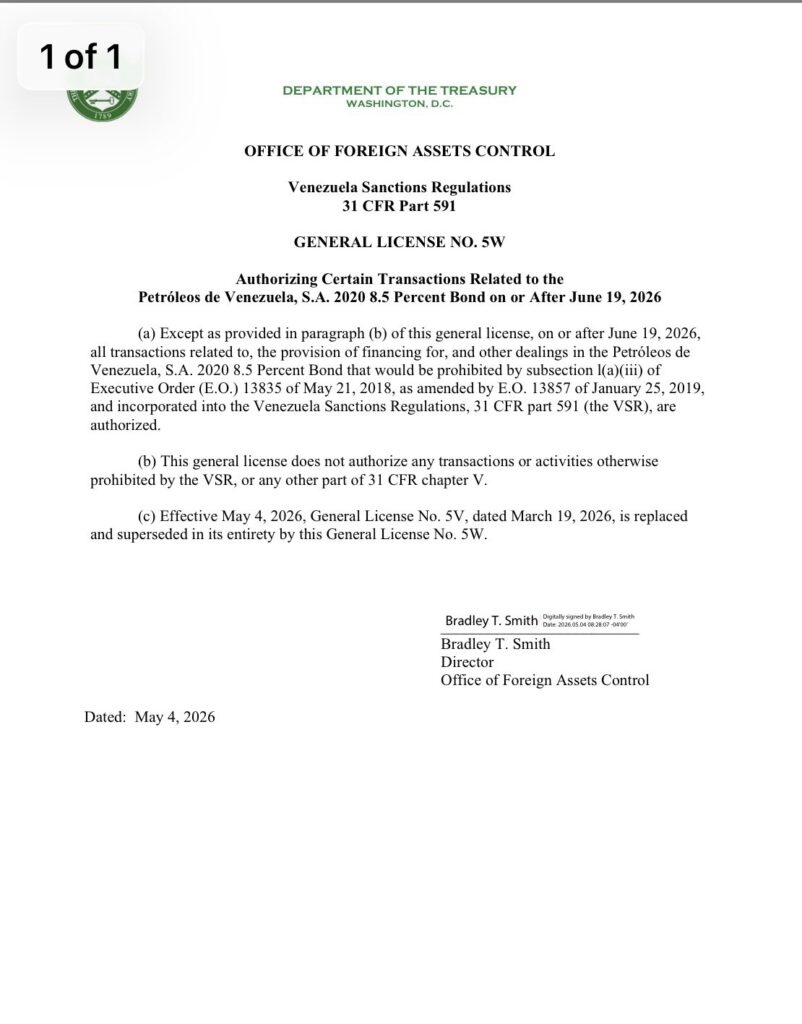

Scope of GL 5W: The CITGO Collateral Clock Is Extended

GL 5W authorizes, on or after June 19, 2026, transactions related to the PDVSA 2020 8.5% bond that would otherwise be prohibited by Executive Order 13835 and the Venezuela Sanctions Regulations. It replaces and supersedes GL 5V, dated March 19, 2026.

The relevant practical effect is that, until June 19, 2026, there remains no general authorization for transactions related to the sale or transfer of CITGO shares in connection with the PDVSA 2020 bond collateral, unless OFAC issues a specific authorization. OFAC’s amended FAQ 595 states that between October 24, 2019 and June 19, 2026, transactions related to the sale or transfer of CITGO shares in connection with the PDVSA 2020 8.5% bond remain prohibited unless specifically authorized by OFAC.

This matters because the PDVSA 2020 bond is tied to one of the most sensitive pieces of Venezuela’s external asset structure: the CITGO ownership chain. Reuters described the license as extending protection for Venezuela-owned CITGO from creditors through June 19, noting that CITGO and its parent companies remain among Venezuela’s most valuable foreign assets and that the Delaware court-ordered sale process still requires OFAC signoff to be fully executed.

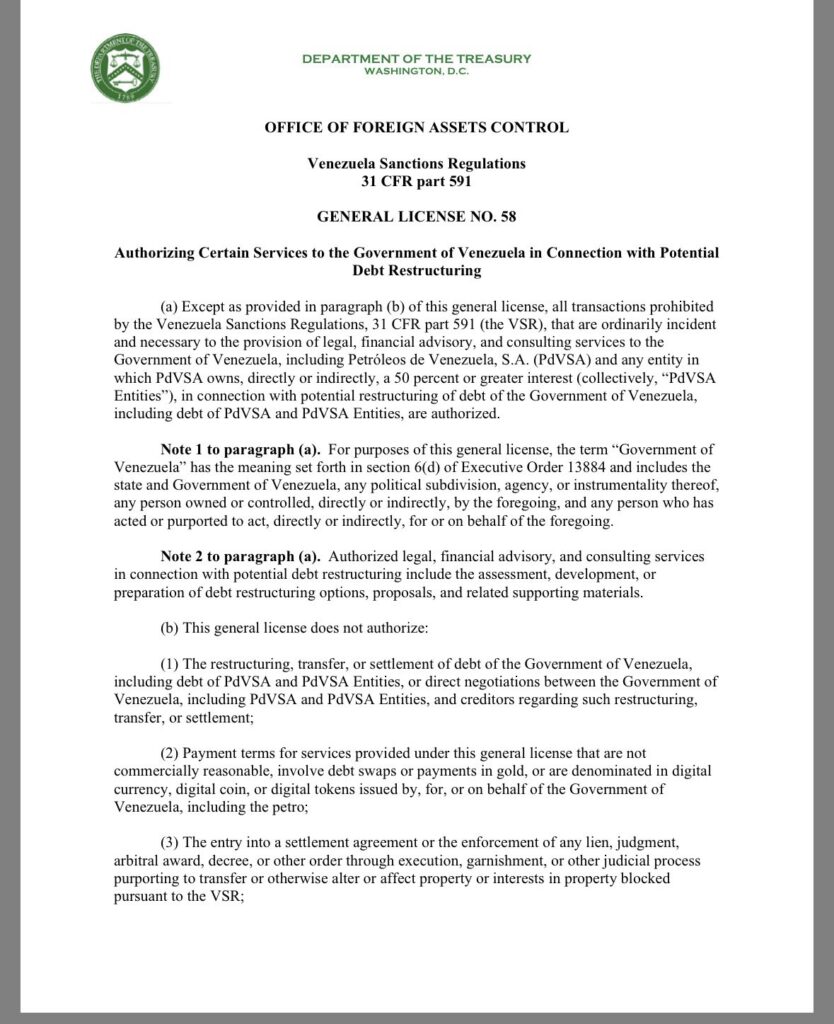

Scope of GL 58: Advisory Work Is Authorized, But Not the Restructuring Itself

GL 58 is the more forward-looking license. It authorizes transactions that are ordinarily incident and necessary to the provision of legal, financial advisory, and consulting services to the Government of Venezuela, including PDVSA and entities in which PDVSA owns, directly or indirectly, a 50% or greater interest, in connection with a potential restructuring of Venezuelan and PDVSA debt. The license specifically includes the assessment, development, or preparation of debt-restructuring options, proposals, and supporting materials.

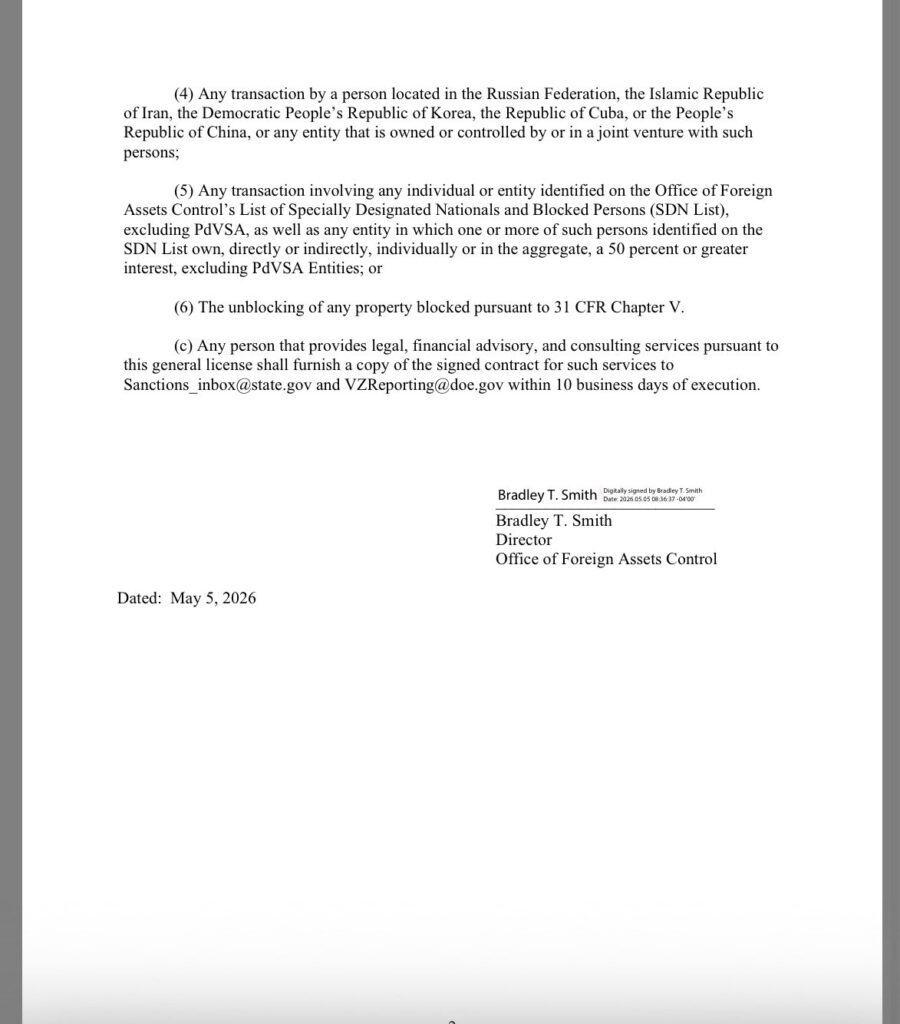

But GL 58 is carefully limited. It does not authorize the restructuring, transfer, or settlement of debt; direct negotiations between the Government of Venezuela, PDVSA, PDVSA entities, and creditors; settlement agreements; enforcement of liens, judgments, arbitral awards, decrees, or other judicial orders; or the unblocking of blocked property. It also excludes payment terms that are not commercially reasonable, involve debt swaps or payments in gold, or are denominated in digital currency or tokens issued by or on behalf of the Government of Venezuela.

The license also excludes transactions involving persons located in Russia, Iran, North Korea, Cuba, or China, or entities owned or controlled by, or in joint venture with, such persons. It further excludes transactions involving SDNs, other than PDVSA and PDVSA entities covered by the license. Service providers must furnish a copy of signed contracts to designated U.S. government inboxes within ten business days of execution.

Strategic Implications: Preparation Without Execution

The two licenses should be read together. GL 5W protects time; GL 58 authorizes preparation. Washington is not allowing a disorderly asset scramble, but it is now permitting the technical architecture of a debt restructuring to be developed.

That sequencing is significant. Venezuela’s debt problem is not limited to sovereign bonds. It includes PDVSA bonds, bilateral obligations, commercial claims, arbitration awards, expropriation claims, supplier debts, litigation pressure around CITGO, and obligations tied to the oil sector and state-owned entities. A fragmented creditor process could undermine Venezuela’s ability to recover economically before a coherent restructuring framework is in place.

GL 58 therefore creates a compliance path for advisers to begin mapping claims, designing scenarios, preparing restructuring alternatives, and developing supporting materials. But the fact that direct creditor negotiations and settlements remain unauthorized means the United States is still keeping the decisive phase under close control.

Note: Leopoldo Martínez’s Anticipated Framework

The new OFAC licenses also give added relevance to the argument Leopoldo Martínez advanced weeks earlier in IQ Latino’s OpEd, “Venezuela’s debt: from default to reconstruction.” Martínez argued that Venezuela’s debt could not be treated as a conventional sovereign restructuring exercise. The issue was not simply how deep the haircut should be, how payments should be rescheduled, or what instruments might restore market access. Venezuela faces not only a debt crisis, but also a collapse of state capacity, an impaired economic model, and a deep erosion of trust. In that context, restructuring must become a tool of reconstruction, not merely a financial negotiation.

In that sense, GL 58 appears to anticipate the kind of preparatory architecture Martínez described: legal, financial advisory, and consulting work can now begin around restructuring options, proposals, and supporting materials. But the license also confirms his caution. OFAC is not yet authorizing settlements, direct creditor negotiations, debt swaps, enforcement actions, or the unblocking of assets. Washington is allowing the design phase of a restructuring while still preventing a rushed or improvised resolution.

Martínez’s warning about CITGO is particularly relevant. Resolving Venezuela’s debt cannot come at the cost of destroying the assets needed for recovery. GL 5W’s extension of protection around the PDVSA 2020 bond collateral fits that logic: it preserves time and leverage so that CITGO is not consumed by a fragmented creditor scramble before a broader restructuring framework is in place.

The market rally following GL 58 therefore reflects more than optimism about creditor recovery. It reflects the possibility that Venezuela’s defaulted debt may be moving from a litigation-driven phase into a policy-managed restructuring phase. Martínez’s earlier conclusion now reads as a useful interpretive frame for this week’s developments: in Venezuela’s case, the central question is not simply how much to pay, but how to rebuild.

Market Reaction: Bonds Rally on the Prospect of a Managed Process

The market read GL 58 as a meaningful signal. Venezuelan and PDVSA bonds rallied after the U.S. authorization of restructuring-related advisory services. Bloomberg Law reported that Venezuela’s sovereign bonds due 2027 rose 1.1 cents to 53.8 cents on the dollar, their highest level in nine years, while PDVSA 2021 notes gained 0.8 cent to 46.3 cents. Reuters-linked market coverage similarly described Venezuelan bonds as rallying after the U.S. authorized Caracas to hire restructuring advisers.

The rally reflects investor expectations that Venezuela’s long-frozen debt market may finally be entering a more organized phase. It also builds on a broader repricing of Venezuelan risk as markets assess the possibility of oil-sector stabilization, renewed institutional engagement, and eventual creditor negotiations under a U.S.-licensed framework.

Still, the rally should be interpreted carefully. GL 58 improves the pathway for preparation, not execution. Bond prices may now reflect a higher probability of eventual restructuring, but the license does not authorize actual settlement, exchange offers, creditor negotiations, or asset transfers. The market is pricing optionality, not a completed deal.

Open Questions

Several core questions remain unresolved.

First, will OFAC eventually authorize direct creditor negotiations? GL 58 allows advisers to prepare restructuring options, but it does not permit the government or PDVSA to negotiate directly with creditors regarding restructuring, transfer, or settlement. A later license or specific authorizations would be required for the next phase.

Second, how will CITGO be treated? GL 5W protects the PDVSA 2020 collateral track through June 19, 2026, but it does not resolve the broader CITGO litigation ecosystem, including judgment creditors, arbitral award holders, bondholders, and the Delaware sale process.

Third, will PDVSA debt be treated separately from sovereign debt? PDVSA’s obligations may require a different structure because they are tied to operating assets, oil revenues, receivables, commercial contracts, and litigation risks. A comprehensive restructuring may need to distinguish between sovereign capacity, PDVSA cash flow, and strategic asset protection.

Fourth, will the restructuring be coordinated with multilaterals? A credible restructuring would likely require macroeconomic assumptions, oil-production forecasts, fiscal projections, and a medium-term recovery plan. Coordination with the IMF, World Bank, IDB, and other institutions may become necessary if the process moves from advisory design to executable settlement.

Fifth, what political framework will support implementation? Venezuela’s restructuring cannot be separated from institutional credibility. Creditors will require enforceability, investors will require rule-of-law assurances, and Venezuelans will require evidence that restructuring supports national recovery rather than another opaque elite bargain.

Bottom Line

This week’s OFAC actions mark an inflection point, but not a resolution. GL 5W keeps the CITGO collateral clock under U.S. control. GL 58 opens a channel for restructuring preparation. Together, they suggest that Washington is moving Venezuela’s debt issue out of paralysis, but only in a sequenced and supervised way.

For markets, that is enough to justify a rally. For creditors, it creates a path toward eventual engagement. For policymakers, it preserves leverage. For Venezuela, it creates an opportunity to shift the debt conversation from default and litigation toward reconstruction.

The key question now is whether this controlled opening becomes part of a broader national recovery strategy. Venezuela does not need a restructuring that simply clears old claims. It needs one that protects strategic assets, restores institutional confidence, supports economic recovery, and helps rebuild the state.